Implementing the Accrued Benefit Cost and Attained Age Normal Methods for Pension Fund Calculations

DOI:

https://doi.org/10.24036/rmj.v4i2.83Keywords:

Pension Fund, Accrued Benefit Cost, Attained Age Normal, Actuarial Liability, Normal ContributionAbstract

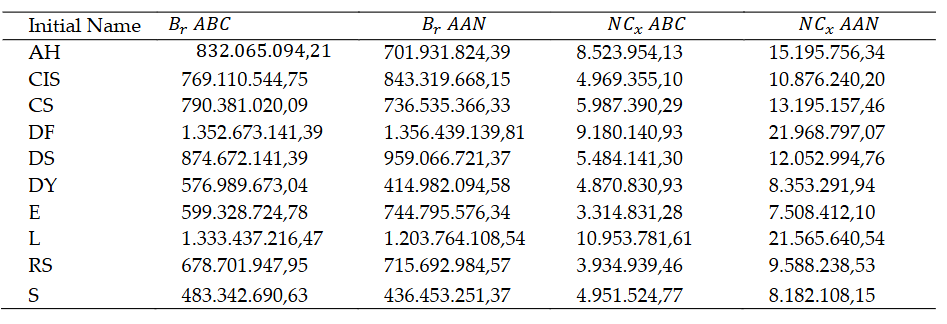

Pension fund management often faces challenges arising from uncertainties in actuarial variables, such as retirement age, years of service, salary levels, and interest rates. Inaccurate calculations may result in fund deficits or impose excessive contribution burdens on companies. This study aims to identify the optimal method for calculating pension funds to ensure the maximization of pension program benefits. The research employs secondary data from a limited liability company, with documentation as the primary data collection instrument. The data include employees’ dates of birth, dates of registration for work, employment commencement dates, and wage records. The analysis focuses on normal contributions, actuarial liabilities, and fund accumulation using the Accrued Benefit Cost (ABC) and Attained Age Normal (AAN) methods. The results indicate that the AAN method generates higher normal contributions than the ABC method, making it more effective in preventing pension fund deficits. Conversely, the ABC method offers a more evenly distributed cost allocation throughout participants’ working periods. The findings suggest that the differences in results between the two methods are influenced by the length of service and the salary levels of participants.